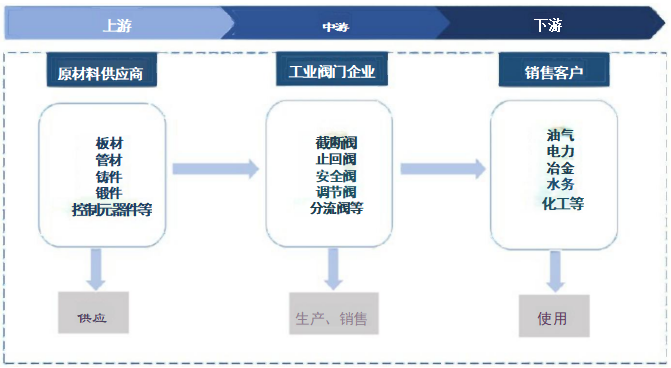

The industrial valve industry chain in China can be divided from top to bottom into upstream raw material suppliers, midstream industrial valve enterprises, and downstream sales customers (see Figure 2-4)

Figure 2-4 China Industrial Valve Industry Chain

The upstream of the industrial valve industry mainly consists of industrial raw material suppliers such as sheet metal, pipe fittings, castings, forgings, and control components. Castings are the core components in the production process of industrial valves, and the production of steel has a direct impact on the price of castings. In recent years, China's steel industry has developed rapidly. According to data from the Stainless Steel Branch of the China Special Steel Enterprise Association, the crude steel production of stainless steel in China reached 25.774 million tons in 2017, an increase of 1.165 million tons year-on-year, or 4.7%. This can provide sufficient and stable raw materials for valve production. Due to the low entry threshold and large number of participants in the upstream industry, the market development is relatively mature, and the product supply is sufficient, resulting in low bargaining power.

The midstream of the industrial valve industry consists of industrial valve enterprises, mainly responsible for the production and sales of industrial valve products. There are numerous enterprises in the industry, fierce price competition, overcapacity in low-end products, and insufficient production capacity and supply of high-end products. According to Sullivan data, raw material costs account for about 70% of valve production costs. The sales price of valve products is usually based on product costs and adjusted according to gross profit margins and changes in raw material prices. If raw material prices rise significantly in the short term, industrial valve companies may not be able to offset or transfer the impact of rising raw material prices on product costs by increasing sales prices. In order to strengthen cost control and better control product quality, leading enterprises in the industry have a strong willingness to penetrate upstream, strong ability to integrate upstream and downstream resources, and can achieve the full coverage of the complete industrial chain from research and development design to raw material production and processing, meeting the requirements of cost reduction, shortened delivery time, and customer review. For example, Neway Corporation has established two valve casting production supporting enterprises, which can produce various carbon steel, stainless steel, and alloy steel castings. This not only provides a stable source of castings for Neway's valve products, but also sets higher quality requirements to meet the needs of high-end customers. Due to the fact that most industrial valve enterprises are engaged in the production and sales of low-end valve products, and the homogenization competition in the low-end valve market is fierce, their bargaining power in downstream industries is generally not high; In the high-end valve market with extremely high product technology content and few competitors, international valve giants and some leading Chinese industrial valve enterprises have strong bargaining power for special valve products such as nuclear power valves.

The downstream industries of the industrial valve industry mainly include oil and gas, electricity, metallurgy, water, chemical and other fields. The fields of oil and gas extraction and transportation, electricity, and chemical applications are the largest areas of industrial valve applications in China, accounting for about 70% of downstream applications (see Figure 2-5). The downstream industry's fixed assets investment and cyclical fluctuations have a greater impact on the demand for valves in the midstream. Since the global economy recovered in 2010, the downstream industry's prosperity has improved and industrial construction has intensified, driving the demand for valve products, further expanding the size of the valve market, giving downstream enterprises in the industrial chain a strong bargaining power.

Figure 2-5 Downstream Application Proportion of Industrial Valves in China in 2017