Development history of China's industrial valve industry

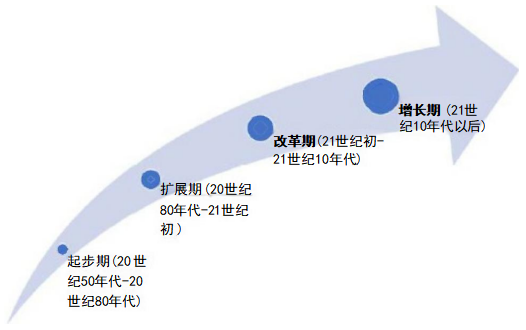

The industrial valve industry in China started relatively late, with over five decades of development since its inception in the 1950s. It has roughly gone through four stages of development (see Figure 2-2):

Figure 2-2 Development history of industrial valves in China

Initial stage (1950s-1980s): In the early 1950s, some mechanical equipment manufacturing factories established by local industrial bureaus under the government began producing industrial valves for urban construction. By the 1960s, due to the needs of national defense construction, the local state-owned Suzhou Iron Factory was renamed "State-owned Factory No. 526", becoming the only nuclear professional valve production base in China. During this period, it provided approximately 420,000 high-quality valves for the first phase of nuclear industry construction and the third-front project, making a great contribution to the construction of China's nuclear industry. During this period, the types and specifications of valve products were relatively limited, mainly because valve manufacturing enterprises at that time lacked the ability to produce high-parameter and high-tech valves.

Expansion period (1980s to early 21st century): After entering the 1980s, China's reform and opening-up continued to deepen, and the industrial system began to learn from international advanced development experience. China's military industrial enterprises gradually realized the transformation from military to civilian, and military valve enterprises also began to independently develop and manufacture complete sets of valve products that meet international standard systems. In order to meet the growing demand for industrial valves in industrial and agricultural construction, some key valve enterprises began to adopt a combination of independent development and the introduction of foreign advanced technology to improve valve technology. Through this approach, China's valve manufacturing level and product quality have been significantly improved compared to before. Since the 1990s, China's domestically produced valve products have begun to enter international markets such as Europe, America, Southeast Asia, and the Middle East.

Reform period (early 21st century to 2010s): Since the early 1990s, China's industrial valve industry has accelerated the pace of modern enterprise management. For example, Suzhou Valve Factory, through resource integration, was listed on the Shenzhen Stock Exchange in 1997, becoming the first listed company in China's industrial valve industry. Subsequently, the company name was changed to "CNNC Sufa Technology Industry Co., Ltd." During this period, China's valve market steadily grew, and valve technology in the petrochemical industry had become relatively mature. Industrial valve enterprises in the industry continuously intensified efforts to develop new markets and new products, laying a solid foundation for the take-off of China's technology industry. In 2008, the US financial crisis erupted, leading to a global economic downturn. This had a negative impact on fixed assets investment in industries such as oil and gas, electricity, and chemical engineering, causing a continuous decline in demand for valves and stagnating market development.

Growth period (after the 2010s): After 2010, the global economy gradually achieved recovery growth, and China's industrial valve industry began to recover, showing a steady upward trend. The number of industrial valve enterprises increased significantly, and a number of enterprises with high-end valve production technology gradually enhanced their competitiveness in the international market. However, overall, the market concentration of the valve industry is low, with a large number of small and medium-sized enterprises, leading to a chaotic market, which poses great difficulties for achieving standardized management in the industry.